0 Comments

Answer:

$1.96

Step-by-step explanation:

The disparity between the delivery price and the actual forward price discounted at the specified discount rate will be the current value.

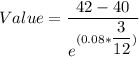

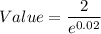

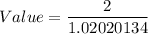

Thus, it can be calculated by using the following formula: